![]()

2020-02-08 調査・研究 Tailwind from Olympics, 0.3% growth TV to grow 0.1% and Internet resumes uptrend

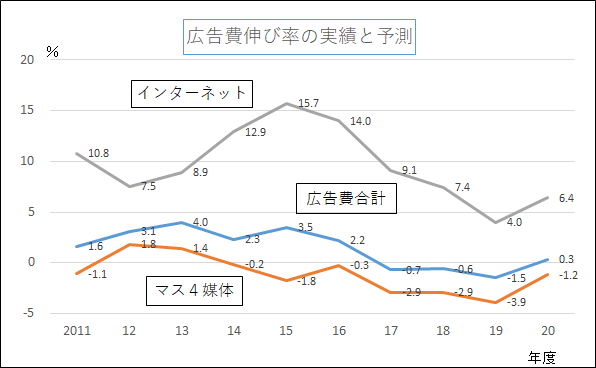

1.5% contraction in FY2019; contraction for three consecutive years

FY2019 advertising expenditure is forecasted to decline by 1.5%, extending the contraction to the third consecutive year. The rate of contraction is accelerating, compared to −0.7% in FY2017 and −0.6% in FY2018. Intensifying trade war between US and China has blunted exports. Furthermore, catastrophes such as typhoon and river flooding between July and September have attenuated corporate advertisements. Sluggish personal consumption due to October consumption tax hike also contributed to the decline.

Phase 1 trade deal was signed between US and China in FY2020. It is expected to ease up trade war’s impact on global economy. In addition, 13 trillion yen of fiscal spending has been included in the country’s FY2019 revised budget and FY2020 budget to combat economic downturn. Although spreading of pneumonias due to the new China’s Coronavirus sparks anxiety, FY2020

advertising spending is forecasted to increase by 0.3% due to confidence in the economy.

By media, TV advertisement is expected to increase slightly by 0.1% in FY2020. Among the 4 medias, TV advertisement is expected to benefit the most from Olympics during July-September period. Businesses have been facing declining spot advertisements in the last year or two. Means to stop the downtrend become the deciding factors. Spot advertisements on radio continue their decline. Radio advertisement’s tailwind provided by specific industries such as law practices and used car sales is expected to wane, bringing FY2020 forecast to −2.2%.

Although newspaper advertisement is expected to benefit from Olympics, the spending is forecasted to decline by 5.5% in FY2020. The rate of contraction is slower compared to FY2019. FY2019 spending was boosted by advertisements related to consumption tax hike, positive growth in July–September period, and high amount of advertisement spending. Magazine advertisement is expected to decline by 9.2%. According to Research Institute for Publications, recovery of comics (independent volumes) boosted FY2019 magazine sales, truncating the decline from −9.4% last year to −4.9%. Weekly magazine sales are expected to continue staying sluggish.

6.4% increase Internet, higher growth rate

In FY2017, Internet advertisements grew by 9.2%, the first single-digit year after 4 years. Growth stayed at 7.4% in FY2018 before decelerating again in FY2019 to 4.0%. Targeted ads read users’ properties with caches and distribute relevant advertisements. Critical voices about these ads are louder. Plus, ads frauds specific to Internet sphere attenuate corporate advertisements. Correlation between Internet advertisements and economic climate is expected to heighten.

However, video advertisements are expected to lead Internet advertisements in FY2020. Following commercialization of next-generation network 5G, corporations are shifting towards video advertisements. FY2020 Internet advertisement is expected to grow by 6.4%, faster than 4.0% in FY2020, thanks to tailwinds such as developing network environment.

Transit advertisement is expected to achieve stable growth of 1.6% in FY2020 too. Although paper mediums are declining, there are more advertisement mediums using digital signages. To prepare for Olympics in this summer, renovations at train stations are expedited, increasing expected digital signage slots. Leaflets and direct mails are expected to contract by 4.4%, at a rate similar to previous fiscal year. Although leaflet’s main customer, the distribution industry, recovered slightly from its slump, other industries such as real estate failed to recover, thus prolonging downtrend of total leaflets. Direct mails continue to stay weak.

This forecast uses the NARI/JCER model developed jointly by NARI and Japan Center for Economic Research. It assumes that changes in advertising expenditure can be explained by domestic economic trends. Two explanatory variables are selected: ordinary profits (operating income plus extraordinary income and expense) published in Ministry of Finance’s Corporate Enterprise Statistics and nominal GDP published by Economic Social Research Institute, ESRI. Forecasted current profits and nominal GDP growth by JCER are plugged in this model to arrive at the forecast value. Overall trend of advertisement expenditure is used to forecast growth rate of each media, including the 4 mass medias of TV, newspaper, magazine, and radio, as well as transit, leaflet, direct mail, and Internet.